I hope this finds everyone well. I have been meaning to post this for over a week now but I have been out with a little back surgery. All is well though and it has given me plenty of downtime to think outside the box a little and develop a few new thoughts and questions. As I will say again at the end of this post, please keep your good questions and ideas coming. Every trade has two sides, and I welcome a good debate of ideas. I think it helps to make us better.

Over the past few week, I have been seeing more and more news and commentary about growing concerns in Europe from policy leaders (might see even more with the disappointing European growth numbers out this week). It seems like views are starting to lean toward support of a weaker Euro (currency). Both of these views have been somewhat confirmed with a few emails with friend across the pond. For more on this, please click on the below links to thoughts from the Financial Times

ECB Preparing To Unleash Unconventional Monetary Policy

All of this has me thinking about what the impact of a weaker Euro would be on European stocks. If support of a strong Euro too boost confidence, moves to support of weak Euro to improve growth, what will impact will this have on future returns for U.S. investors?

Yesterday, I did a little informal survey of among some senior contacts I have at large firms (UBS, Barclays, Morgan Stanley, JPM, Goldman, etc). When discussing their views on European equities, I found that all were still using terms such as “positive”, “increasing allocations as compared to other areas”, “”flows are strong so we are maintaining our overweights”, and my favorite, “flows are strong and people are desperate for income, so we will maintain our overweight”

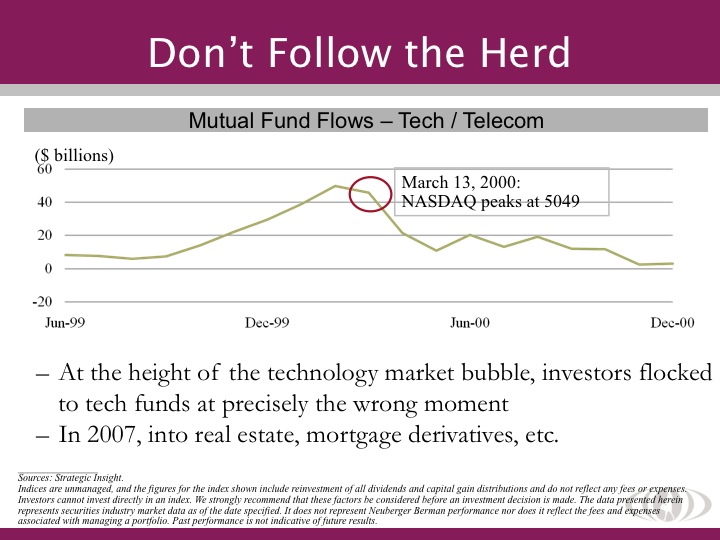

Investor flows and strong consensus tends to not be good leading indicators for future return (remember flow to tech fund in the late 90s and flows to mortgages and mortgage derivatives just before the 2009 crisis, etc.). Also, lets not forget an investment industry favorite, past returns are not good indicators of future results (flows tend to follow hot returns at the wrong time). Below is a chart that I have been using in talks to a women’s group Harvard, Smart Woman Securities, for many years.

If the Euro is driven weaker by talk of policy makers or market participants, won’t this be a drag on European stock returns for U.S. investors? I think it could.

At the very least, I hope this is debated more. As I have posted before, I wish more debate like this would happen in front of clients. How about more transparent discussions of both side of a trade with clients and a focus on comfort and peace of mind (see my past post – “Are We Spending Too Much Time Selling Alpha?”)

The following is the only link I have found so far from some industry leaders on the potential future impact of the Euro as it related to the return potential of European stocks: What an “Overvalued” Euro Means for European Equity Allocations.

Versus following consensus, it might be good to take a few chips off the table as it relates to European stocks.

As promised above, please send your thoughts. Feedback and debate is always welcome!